What is Buy Now Pay Later?

March 16, 2024, 5 min read

Buy Now Pay Later (also known as BNPL) is a new trend that has evolved in the world of consumer finance during the past several years. The convenience and adaptability of this method of payment have contributed to its meteoric rise in popularity among consumers. In the following paragraphs, we will discuss what “Buy Now Pay Later” is, how it operates, and its potential influence on credit ratings, with a specific emphasis on the market in the United Kingdom (UK).

What is “Buy Now Pay Later”?

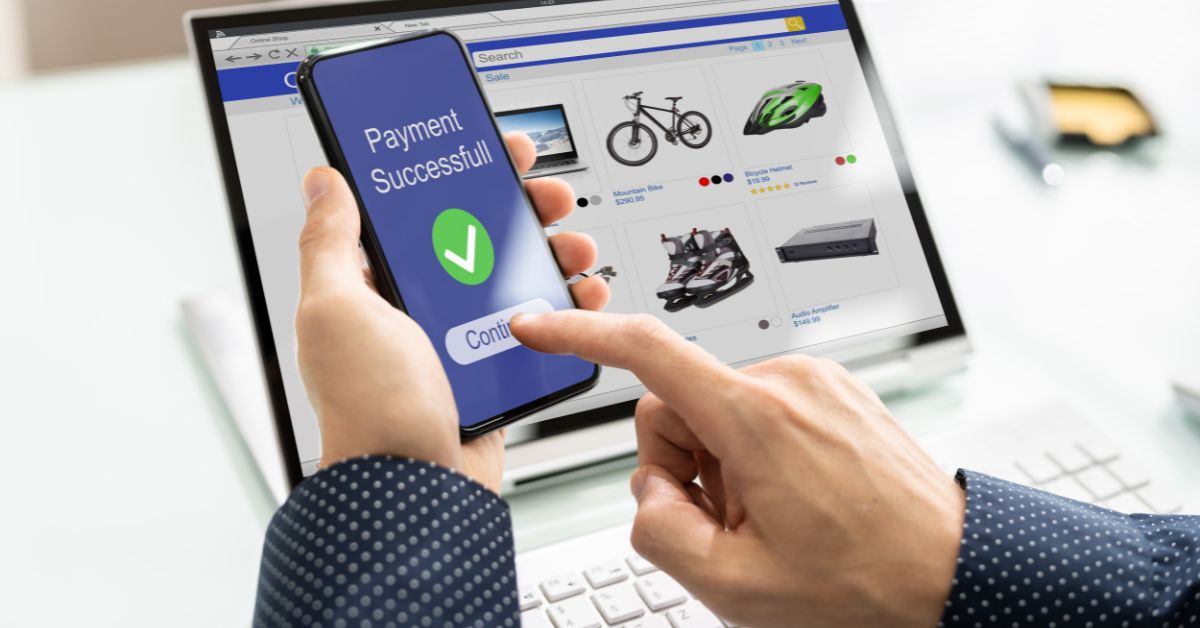

Buy Now Pay Later is a payment option that allows customers to buy products or services right away while delaying the payment for some time. In contrast to conventional loans or credit cards, in which interest is charged on a rolling basis, BNPL services often come with an interest-free grace period. This appeals to customers who are looking for flexible payment choices that don’t require them to pay any upfront charges right away.

How Does it Work to Buy now and Pay Later?

Customers who shop either in-person or online have the option to use a Buy Now Pay Later service when they check out of their purchase. This choice is provided to them at the checkout. Klarna, Clearpay, Laybuy, and PayPal Credit are examples of well-known BNPL service providers.

Application and permission: In order for clients to make use of BNPL, they are need to apply for permission, which is typically a straightforward process that entails submitting personal information such as their name, address, and job status. Because the decision regarding permission is frequently made immediately, this choice is one that is both convenient and easy to access.

Customers who have been pre-approved can break up the total cost of their purchase into many, more manageable payments exempt from interest charges. These payments are made over the course of a predetermined time period, which can range anywhere from a few weeks to many months depending on the terms set forth by the BNPL provider and the retailer.

payback Schedule: It is absolutely necessary to stick to the payback schedule in order to prevent late penalties or any other costs that may be incurred. Some of the services provided by BNPL also give consumers the option to make early repayments without incurring any additional fees.

The absence of interest charges throughout the interest-free period is one of the primary selling features of the products and services offered by BNPL. This is true in the majority of cases. However, it is essential for customers to have a thorough understanding of the terms and conditions, as certain service providers may charge interest fees if payments are not completed within the time period that was originally agreed upon.

What Happens to Your Credit Score When You Buy Something Now and Pay Later?

Concern about the effect of “Buy Now, Pay Later” on a consumer’s credit score is understandable and common. The following is an explanation of how BNPL can affect credit scores:

Credit Checks

When a client applies for a BNPL service, the provider may perform a light credit check on the application in order to determine whether or not the client is creditworthy. A gentle inquiry into one’s credit history does not have any adverse effects on the credit score. However, lenders may become concerned if a borrower makes multiple applications for BNPL services, which may have a negative effect on the borrower’s credit score.

Incomplete Payments

Even though BNPL services do not charge interest during the interest-free period, payments that are late or that are not made at all can have a negative impact on credit scores. It’s possible that some BNPL suppliers will record late payments to credit bureaus, which can result in a lower credit score for the user.

Borrowing Capacity

Using BNPL services on a consistent basis and in a responsible manner can show potential lenders that a consumer is capable of responsibly managing credit. This may have a beneficial effect on creditworthiness and may, in the future, boost one’s capability for borrowing money.

The urge to make several purchases without fully contemplating the financial ramifications is one of the potential problems that can be associated with BNPL. This can lead to an accumulation of debt. Building up an excessive amount of debt through BNPL services might put a strain on one’s finances and have a bad impact on one’s credit score.

In the UK, you can “Buy Now and Pay Later.”

The use of BNPL services has experienced a substantial uptick in demand across the entirety of the United Kingdom. Consumers now have more choice and control over how they can most effectively manage their purchases as a result of many merchants in the UK offering BNPL alternatives at the checkout. The product’s simplicity, the rapidity with which it can be approved, and the absence of interest during the period in which the loan is interest-free have all contributed to the broad adoption of BNPL in the UK.

The Benefits of Making a Purchase Now and Paying Later

BNPL services allow consumers to delay payments, making it simpler to manage one’s finances in the event of unanticipated costs or crises.

The interest-free term that is provided by BNPL services can be beneficial, particularly for those individuals who are able to repay the loan within the agreed-upon time frame.

Flexibility is one of BNPL’s most enticing features, since it enables customers to make purchases without immediately placing a strain on their finances, making the service a good choice for people whose income is inconsistent.

When applying for BNPL services, a soft credit check is normally required; however, this type of check does not have an effect on applicants’ credit ratings in the beginning.

Negative aspects of the “Buy Now, Pay Later” Model

Fees for Late Payments If you do not make your payments when they are due, you may be subject to late fees. These penalties can mount up over time, which drives up the total cost of the transaction.

Possible Accumulation of Debt The simplicity of using BNPL could encourage impulsive spending, which could lead to excessive debt if it is not managed appropriately.

Repeated late payments or extensive use of BNPL services can also negatively influence a person’s credit score.

Conclusion

Buy Now, Pay Later is quickly becoming one of the most popular and simple payment options available to customers in the UK. Because of its adaptability and its interest-free periods, it is an appealing alternative to conventional loans and credit cards. However, it is vital for customers to use the services provided by BNPL in a responsible manner, according to repayment schedules to avoid incurring late fees and perhaps damaging their credit scores.

As BNPL continues to develop, it is essential for customers to keep themselves informed about its terms and conditions and evaluate whether or not it is appropriate for them based on their own personal financial situations. The prudent management of one’s financial situation can benefit from using BNPL, which can be a useful tool; but, just like with any other type of financial service, it takes careful thinking and responsible decision-making.